The long awaited and much contested DOL Rule imposing a fiduciary duty on brokers providing advice to retirement accounts is now final. Though it provides a significant runway for implementation (at least a year), the Rule is already changing business models from small brokerages right up to the biggest wirehouses.

The Big Change

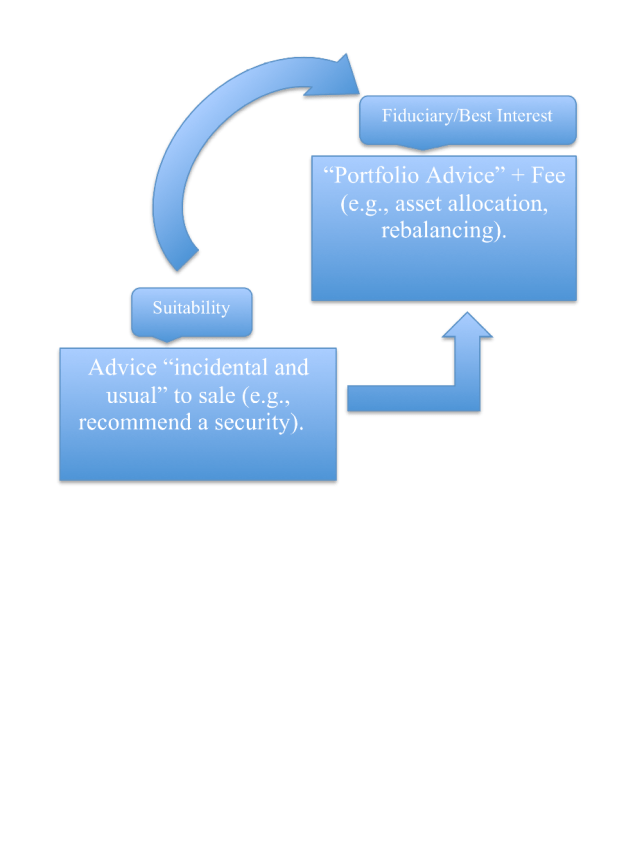

Under current rules, brokers, for the most part, operate under a standard that only requires advice to clients to be suitable, but not necessarily in the client’s bests interests. Investment advisers, by contrast, are always operating under a best interests fiduciary duty standard.

The DOL, with strong support from the White House, has moved to plug this gap by using its powers to issue a best interests standard for ALL advisers providing advice over retirement plans. (Such plans are defined as 401(k)s and other employer-sponsored plans, IRAs and other tax-deferred accounts, such as health savings accounts.) The Rule is supposed to provide increased protection for retail investors, who the DOL says are more likely to use brokers on commission than their more expensive counterpart – investment advisers paid as a percentage of assets under management.

While it was already the case that brokers providing repeated investment advice (e.g., asset allocation and rebalancing advice) for a fee had a fiduciary duty, the new DOL Rule broadens the definition to include even one-time investment consultations or recommendations. Rollover recommendations also would be considered fiduciary advice.

Potential Impact

The potential impact on brokerage houses and their representatives is immense. For one thing, investors who bring suit or arbitrations against their representatives will have a broader claim basis – representatives could be personally liable for losses caused by a breach of the best interests duty.

Fiduciaries also are subject to potentially large excise taxes for engaging in prohibited transactions, unless they qualify for an exemption. ERISA currently prohibits fiduciaries from completing transactions that involve conflicts of interest unless they disclose the conflicts and operate under the oversight of an independent fiduciary.

Commissions/Annuities Still Ok

The Rule permits brokers to charge commissions provided they comply with the Best Interest Contract Exemption (BICE) and other requirements. BICE permits a firm to charge commissions if the adviser and the client enter into a contract that specifies that all advice be in the best interests of the client, clearly discloses all conflicts, directs the customer to a webpage disclosing the compensation arrangements entered into by the adviser and firm, and makes customers aware of their right to complete information on the fees charged. In addition, broker-dealers will need to have procedures in place to encourage advisers to make recommendations in the client’s best interests.

Finally, there was industry concern that the sale of certain financial products considered to be riskier or more expensive than others (i.e., annuities, insurance, and mutual funds) on commission would have been barred under the Rule. However, the Rule permits such sales under the BICE.